It has been almost three years now since WeGroup focused on developing technology that helps insurance intermediaries digitalise and simplify their advice and distribution processes. No obvious task in a robust and conservative sector. The Ghent-based technology company has had to reinvent itself several times to meet its customers' needs. We spoke with WeGroup CEO Arvid De Coster about evolving market trends and ambitious plans for the future.

A product of everyone

"I can still picture us there. Three motivated young guys and a set of white plastic garden furniture in a dusty attic room," Arvid De Coster, CEO and one of WeGroup's founders, looks back nostalgically. "A lot has changed since. Not only because WeGroup now has almost fifty employees and was thankfully able to say goodbye to garden furniture as office furniture long ago, but also the evolution our platform went through over the past years. An evolution driven mainly by the market: by our group of now more than 600 broker clients, as well as by partners and fellow insurtechs. When people sometimes ask me whose idea WeGroup was, today it is impossible to attribute that to one single person. Our technology is the result of evolution through so many factors. Iteration after iteration, and where necessary even switching approach entirely. The platform is a product of the market and all the players in it. WeGroup belongs to all of us."

From digital broker to a platform for intermediaries

At the end of 2017, WeGroup started out as a digital broker. A year and a half after its founding, however, the decision was made to switch approach and fully commit to supporting intermediaries.

"Of course, that change of course was one of the most important moments in our company's history. We had always focused on digitalising and simplifying insurance distribution, but it became clear to us that we could create much more impact by helping the established providers, intermediaries in particular, achieve that goal. It was then, in early 2019, that the ball really started rolling," De Coster explains.

"In that new phase, we went looking for what the broker needed to save time and so focus more on where they make the difference: personal service and tailored advice. That is how we arrived at our first core functionality: multi-tarification. A simple concept in which the user enters a minimum of information to get a comparison on price and quality for the insurance products of different companies. A game changer with major time savings as a result, or so we thought."

Multi-tarification no longer the foundation

Today, almost three years later, WeGroup sees this entirely differently. For them it is clear that multi-tarification will not make the difference for the broker. According to Arvid there are several reasons for this.

"First, comparing different products on price and quality is not a standard part of the advice process for many intermediaries. Many brokers can draw on years of experience and extensive product knowledge. After a conversation with a customer, they can often perfectly assess where to find the most suitable coverage at competitive rates. Price plays less of a role there in itself, since real 'price shoppers' will increasingly find what they want online anyway."

"Furthermore, at WeGroup we strongly believe that tailored advice also comes with a broad range of tailored products. Multi-tarification saves time when standard products are compared with each other, for example two simple fire policies with similar additional coverage. But what if that standard offering is no longer sufficient? In the future we will see ever more diversification in product offerings within the established companies, supplemented in the market by the offerings of new players such as specialised underwriters, MGAs and so-called 'neo-insurers'. In all these cases, the usefulness of the one-to-one product comparison as we offer it today is outdated."

Digital advice conversation

If the angle of product comparison is not what the brokerage needs, then we naturally ask ourselves what can make the difference. WeGroup has clearly thought about that too.

"The basis remains the same for us: digitalising and simplifying advice and insurance distribution. Giving intermediaries the tools to grow their portfolio effectively and manage it optimally. To respond to current market trends, however, and to bring our platform in line with our predictions for the future, we have completely redefined our product vision. That happened a year ago, with the result that over the past twelve months we have worked hard behind the scenes on new applications, which we will launch in several phases."

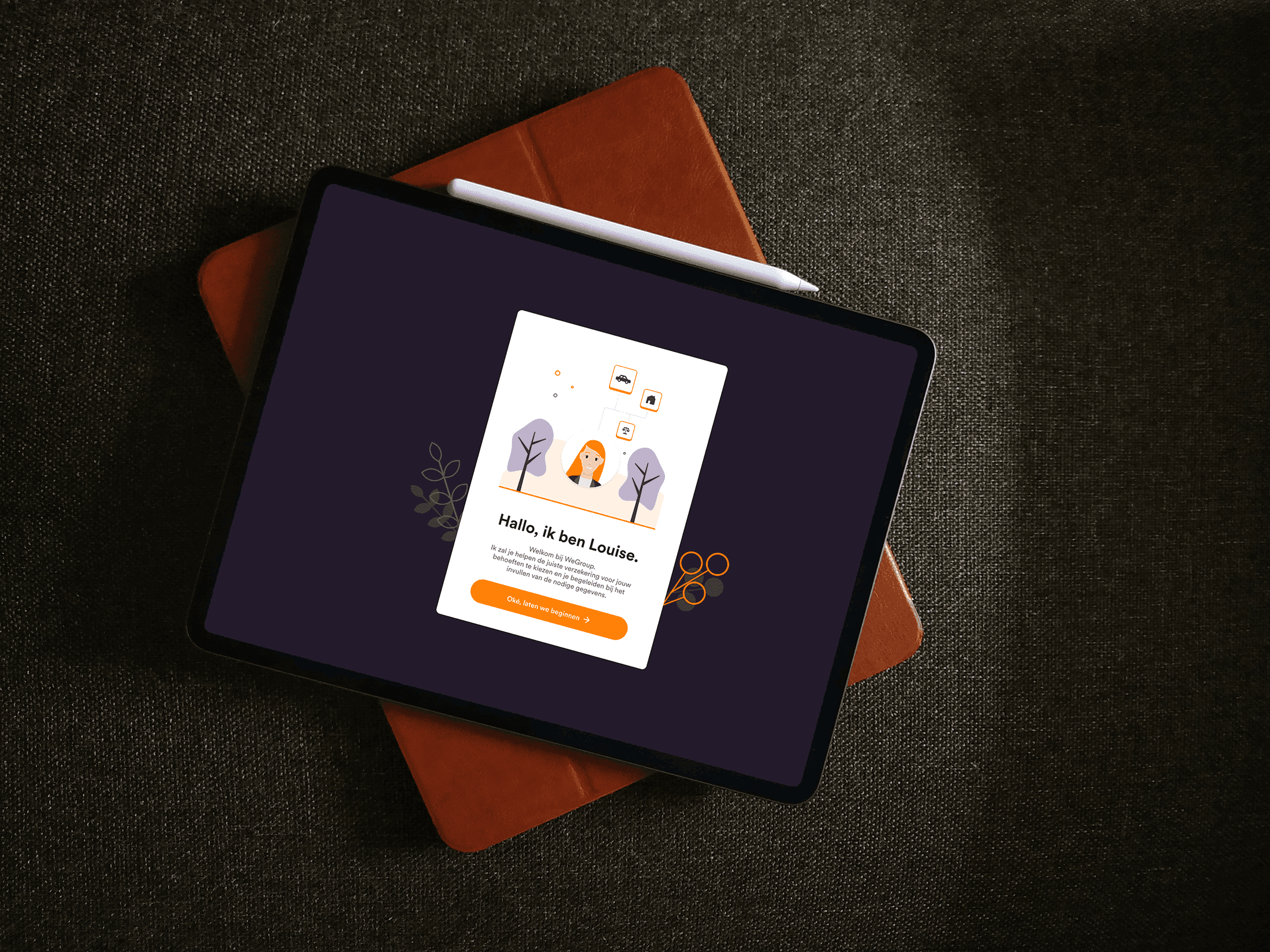

"Concretely, the first step is the roll-out of a completely new Digital Advice conversation. By stepping away from multi-tarification as the core functionality, we were able to shift our angle from a 'product focus', where the broker starts from a product type to arrive at the best terms and premium, to a 'customer focus', which starts from the customer's needs and risks. The outcome of this advice conversation is therefore not necessarily a specific insurance policy or premium, but a comprehensive advice report that maps the customer's profile and gives the broker suggestions on which product types match that profile."

"What is also interesting is that the broker can deploy this functionality fully adapted to the office strategy. The Digital Advice conversation can be used in a hybrid way, together with the customer, or placed on the website to put the customer at the controls in a fully digital experience. Finally, the broker can also integrate the module into the operations of partners to collect leads through, for example, car garages, bicycle shops or real-estate agents."

Besides the Digital Advice conversation, WeGroup has many more big plans. According to Arvid, the ambition has never been greater. We are certainly very curious about what the future will bring for WeGroup and the wider insurance landscape.